Part 2 – How Quickly Can you Boil a Frog? – Why we should still think about inflation

During the 19th century, several German and American scientists undertook experiments observing the reaction of frogs to slowly heated water. Without exploring the detail of the experiments or the debate over their scientific validity, they spawned the parable about a frog being boiled alive if cold water were heated at a sufficiently slow rate that the frog failed to adjust to its changing circumstances.

At Ardea IM we think about inflation somewhat like the frog parable – it is that persistent and gradual feature of the fiat money system that ‘melts’ the purchasing power of our money over time. But that’s not the end of the story. We believe inflation still presents a risk for three reasons:

- In a low interest rate world, inflation expectations as measured by inflation linked securities are dramatically below long-term historical norms. This creates a risk that even small spikes in inflation can have an outsized negative impact on investors’ portfolios given record low interest rates amplify volatility.

- Inflation, when measured as a proportion of investors’ total expected returns, is enormously hard to predict.

- Low recent inflation releases have been heavily influenced by cyclical factors which could rebound quickly.

Why is inflation volatility relevant in a world of benign inflation?

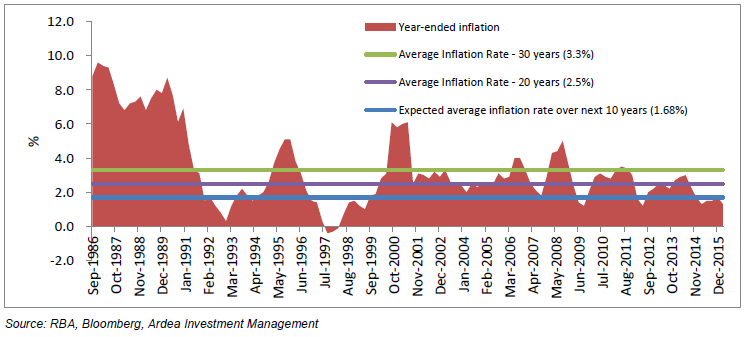

With inflation hitting its lowest rolling year-end point of 1.0% since September 1998, a contributor to the Reserve Bank cutting interest rates to a record low of 1.5% in August 2016, it appears many investors are unconcerned with the impact of inflation on their portfolios. Current market expectations of inflation are remarkably naïve when viewed in a historical context, with the Australian inflation linked bond market expecting average inflation over the next 10 years to be just 1.68%1 p.a. compared with typical realised inflation rates over 2.5% in decades past. This is largely informed by the recent inflation data releases.

The fact is that inflation for the quarter ending in March 2016 was -0.2% and in the subsequent June quarter rebounded to a positive 0.4% result, illustrating how inflation can change substantially in the short-term, which in turn influences expectations over the long-term.

To many, this seems inconsequential, but what this highlights to us at Ardea IM is that we are entering into a new period of volatility. Small differences in expectations versus realised outcomes can have larger impacts than periods where global interest rates were much higher and investors had more yield ‘cushion’.

Furthermore, many investors fail to appreciate that whilst the absolute level of inflation is low, it is very hard to predict what your real return (i.e. your return over and above inflation) will be on money invested in yield- producing investments for a given period, particularly on new money being invested in markets at current low yields.

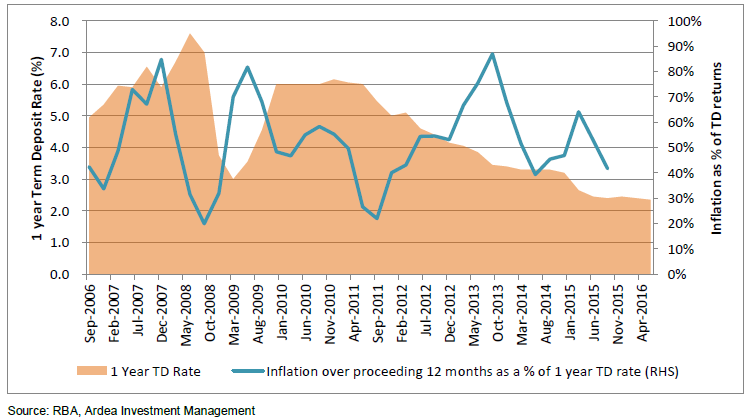

The following graph shows historical 1-year term deposit rates every quarter over the last 10 years (the shaded part) and then the percentage of the return of that term deposit rate absorbed by inflation over the next 12 months. As you can see, this varies significantly, with some years seeing nearly 90% of average term deposit returns absorbed by inflation, and this was in periods where interest rates were much higher than they are now. This highlights just how unpredictable real returns over and above inflation can be.

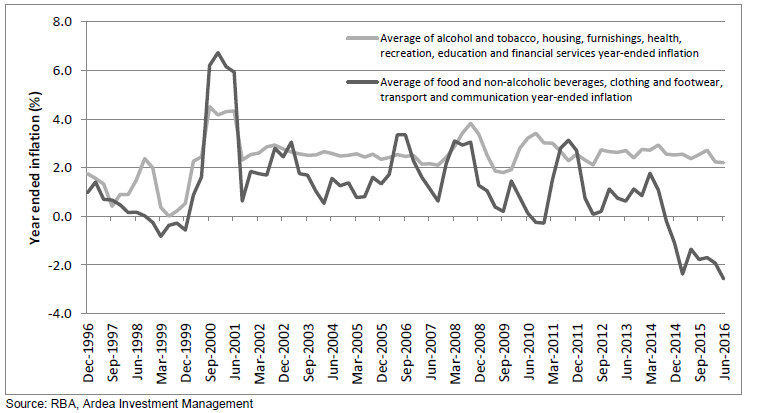

Finally, when we drill down into the component parts of inflation, we observe that the downward pressures on prices over the last two years have been due to a few core areas, which could quite easily and quickly increase:

- Petrol prices and transport costs have fallen on the back of the crash in oil prices due to oversupply from the OPEC producers in an attempt to drive marginal US shale oil producers out of the market. This market is slowly returning to more balanced global demand and supply and as such, oil prices are creeping

- Communication costs are being driven ever lower by free communication products like social media and messaging

- Clothing and grocery costs have fallen due to the entry of large foreign competitors like Aldi and Zara, which have put considerable pricing pressure on domestic

These headwinds have resulted in substantial downward pressure on the prices of many common household ‘basket items’ but like all cyclical factors, they can rebound quickly. The headline inflation figure also hides the fact many large household expenditure groups such as housing costs (i.e. rent), health care, education, alcohol and tobacco, as well as financial services and insurance continue to appreciate steadily in price.

Conclusion

Like the parable of the frog being boiled alive slowly and not noticing until it is too late, investors need to be constantly wary of the continuous impact of inflation on the spending power of their portfolio returns. We challenge investors to think about the risks of inflation volatility on their broader portfolios, despite the long- term cyclical down-trend in current and expected future inflation in markets. Inflation outcomes are very hard to predict year to year, have the potential to change quickly, and can consume a large part of returns in a low-yielding world. We haven’t yet seen the tail risk inflation shock potential of all of the stimulatory monetary policy over the past few years either.

Don’t write off inflation just yet, it still has the potential to cook investor returns.

By The Ardea Investment Management Team & Samuel Morris, CFA (Investment Specialist, Fidante Partners)

1) Australian Inflation Linked Bond (ILB) 10-year breakeven inflation rate from Bloomberg on 5 August 2016. The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.